Trusted partner for insurance companies around the world:

Our AI models are used worldwide

1,500%

Average ROI

to Customers

19

Countries deployed

Winner of Global Awards

8

Years in the

Market

30,000,000+ policies analyzed

Leading European AI motor insurance

analyzer

3

Data Science

Teams with 20% PhDs

AI tools for actuaries to adjust existing Risk Models by finding hidden patterns

Working closely with pricing teams to optimize pricing and adjust risk predictions

Discover more

Revolutionizing

sales and marketing dynamics

Gain Instant LTV-predictions and streamline lead qualification processes for unparalleled success

Discover more

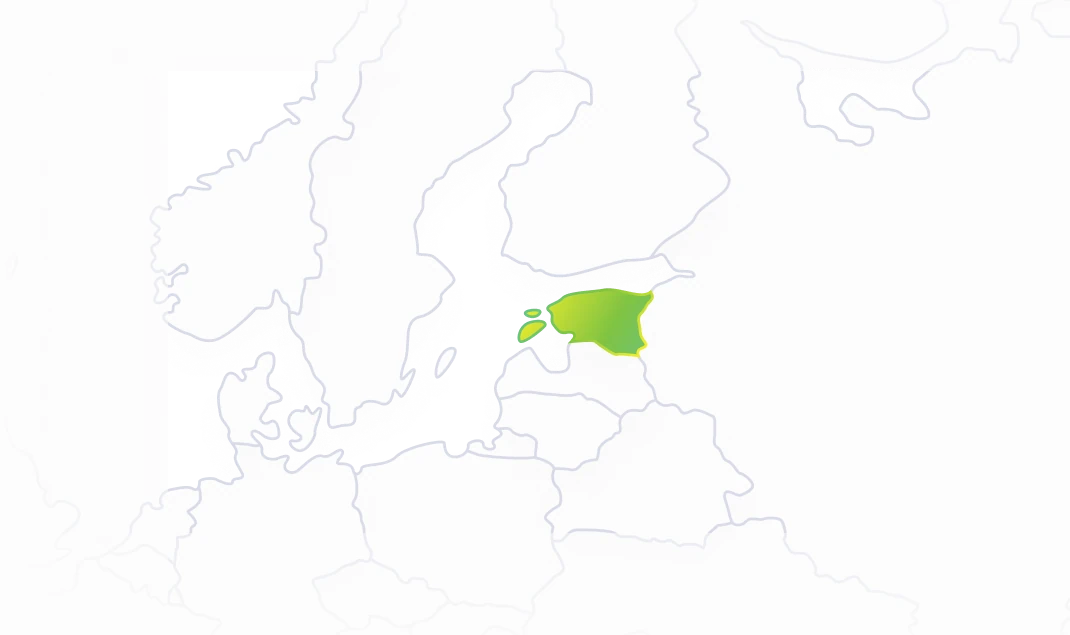

Breaking New Ground:

our AI-driven risk prediction expands into Estonia!

Go-live with our first Estonian client within 3 months,

are you ready to be the next one?

What our clients say about us

Join our esteemed clientele and experience what technology can do for you

The figures from K2G convinced us in the proof of concept and we therefore decided to use AI technology in our pricing to be able to make the best offer to the best customers

In collaboration with K2G, Balcia's got data-driven insurance that's all about you. More than 800 factors, from crash tests to local traffic, are considered for a smarter approach.

At K2G, we're dedicated to making insurance more accessible, transparent, and customer-centric. This expansion into Azerbaijan aligns perfectly with our vision, and we're excited to embark on this journey with Qala Insurance.

Connect with us in your language

Locate your representative for seamless communication and support.

Michael Bachl

Director Market Relations

Andreas Steiner

Senior Director

.png)

Jon Kirk

VP Business Development UK

Aline Schillig

Senior Actuarial Advisor

.png)

Ida Nurhaeni-Gohla

Director Business Development

Michael Bachl

Director Market Relations

Olena Horshkova

Senior Expert Actuary and Underwriter

Ida Nurhaeni-Gohla

Director Business Development